ACA Subsidies 2026: What 85% of Americans Can Expect

The landscape of healthcare in the United States is constantly evolving, and a significant component of this evolution revolves around the Affordable Care Act (ACA) and its associated subsidies. As we look ahead to 2026, a staggering 85% of Americans are projected to be eligible for some form of financial assistance to help them afford health insurance through the ACA marketplaces. This represents a monumental effort to make healthcare more accessible and affordable for a vast majority of the population. Understanding these ACA subsidies 2026 is crucial for individuals and families seeking to navigate their healthcare options effectively.

The ACA, often referred to as Obamacare, was enacted in 2010 with the primary goal of expanding health insurance coverage. A key mechanism for achieving this goal involves subsidies, which come in two main forms: Premium Tax Credits (PTCs) and Cost-Sharing Reductions (CSRs). These subsidies are designed to lower the monthly cost of insurance premiums and reduce out-of-pocket expenses like deductibles, co-payments, and co-insurance. The expansion of eligibility and the increased generosity of these subsidies, particularly under recent legislative changes, have significantly broadened their reach, bringing the 85% figure into sharp focus for ACA subsidies 2026.

For many years, the ACA offered subsidies to those earning between 100% and 400% of the Federal Poverty Level (FPL). However, the American Rescue Plan Act (ARPA) of 2021 and subsequently the Inflation Reduction Act (IRA) of 2022 dramatically enhanced these subsidies. These legislative changes eliminated the income cap for subsidy eligibility and increased the amount of financial help available, ensuring that no one pays more than 8.5% of their household income for a benchmark silver plan. These enhanced subsidies are currently set to expire at the end of 2025, making the discussion around ACA subsidies 2026 particularly pertinent as policymakers debate their extension or modification.

This comprehensive guide will delve into what 85% of Americans can expect from ACA subsidies 2026. We will explore the eligibility criteria, how subsidies are calculated, the different types of financial assistance available, and practical steps you can take to ensure you are maximizing your savings. Whether you are currently enrolled in an ACA plan, considering enrollment, or simply want to understand the future of affordable healthcare, this article will provide valuable insights into the dynamics of ACA subsidies 2026.

Understanding the Basics of ACA Subsidies

Before we dive into the specifics of ACA subsidies 2026, it’s essential to grasp the fundamental concepts behind these financial aids. The ACA marketplace, also known as the health insurance exchange, is a platform where individuals and families can shop for health plans. These plans are categorized into metal tiers: Bronze, Silver, Gold, and Platinum, each offering different levels of coverage and cost-sharing.

Premium Tax Credits (PTCs)

Premium Tax Credits are the most common form of ACA subsidies 2026. These credits reduce the amount you pay each month for your health insurance premium. They can be paid directly to your insurance company, lowering your monthly bill, or you can claim the full credit when you file your federal income taxes. The amount of your PTC depends on several factors, including your household income, household size, and the cost of the second-lowest-cost silver plan available in your area.

Crucially, the enhanced subsidies introduced by ARPA and IRA ensure that individuals and families at all income levels can qualify for PTCs if they purchase coverage through the marketplace and meet other eligibility requirements. This means that even those above 400% FPL, who were previously ineligible, can now receive assistance if the cost of the benchmark plan exceeds 8.5% of their income. This expansion is a key driver behind the projection that 85% of Americans could benefit from ACA subsidies 2026.

Cost-Sharing Reductions (CSRs)

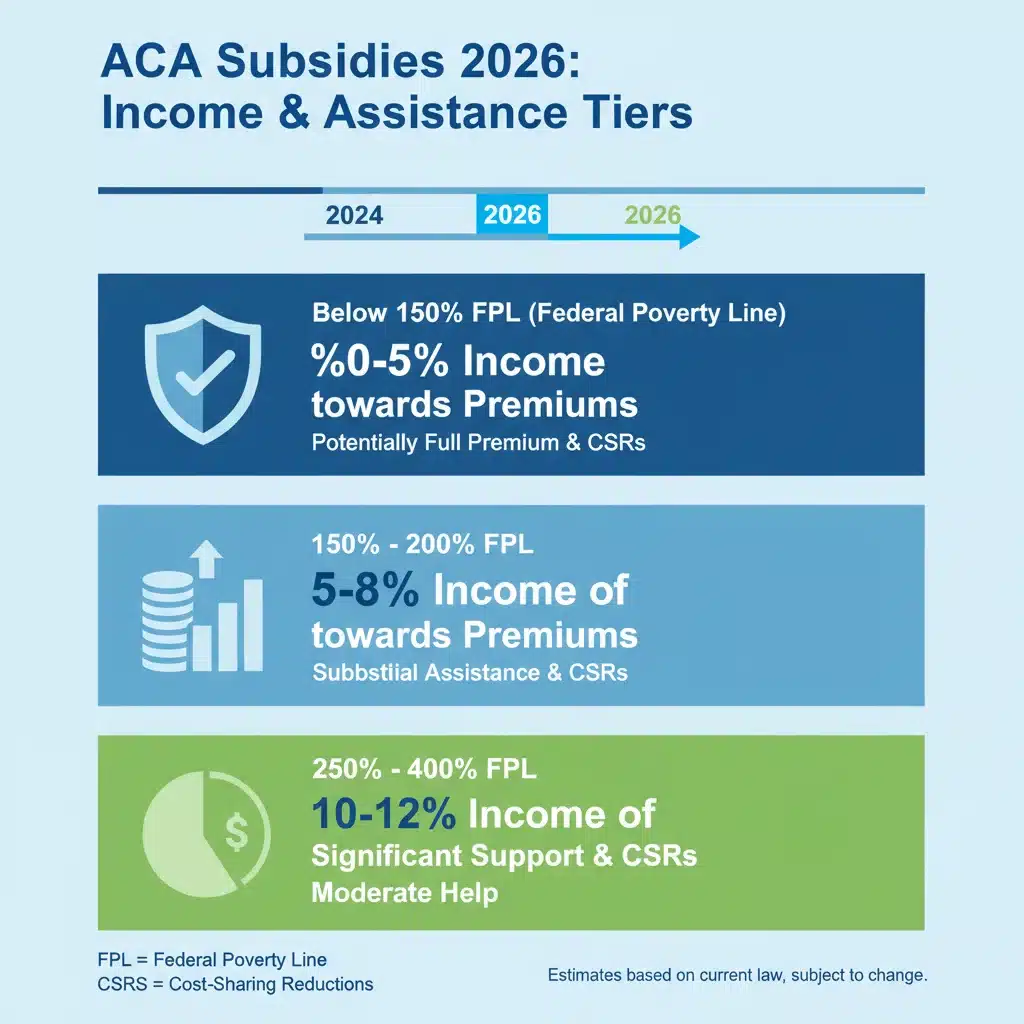

Cost-Sharing Reductions are another vital component of ACA subsidies 2026, though they work differently from PTCs. CSRs reduce the amount you have to pay out-of-pocket when you use your health insurance, such as deductibles, co-payments, and co-insurance. Unlike PTCs, CSRs are only available if you enroll in a Silver-tier plan. They are also tied more directly to income levels, generally available to those earning between 100% and 250% of the FPL.

When you qualify for CSRs, your Silver plan effectively becomes more generous, offering benefits similar to a Gold or even Platinum plan at a lower premium. This makes Silver plans particularly attractive for those who qualify for CSRs, as they receive significant financial protection against high medical costs. The interplay between PTCs and CSRs is fundamental to understanding the comprehensive support offered by ACA subsidies 2026.

Eligibility for ACA Subsidies in 2026

To qualify for ACA subsidies 2026, several criteria must be met. While the enhanced subsidies have broadened eligibility, the core requirements remain:

- Income Level: Your household income must fall within a specific range relative to the Federal Poverty Level (FPL). Under the enhanced subsidies, there is no upper income limit, as long as the benchmark plan costs more than 8.5% of your income. For CSRs, the income limit is typically 250% FPL.

- Household Size: Your household size, which includes you, your spouse, and anyone you claim as a tax dependent, impacts your FPL calculation and thus your subsidy amount.

- No Access to Affordable Employer-Sponsored Coverage: You generally cannot be eligible for subsidies if you have access to affordable health insurance through your employer or a family member’s employer. Employer coverage is considered affordable if the employee’s share of the premium for self-only coverage is no more than 9.12% (for 2023, subject to annual adjustment) of their household income.

- No Eligibility for Government Programs: You are not eligible for Medicare, Medicaid, or CHIP.

- Lawful Presence: You must be a U.S. citizen or lawfully present immigrant.

- File Taxes Jointly (if married): If you are married, you must file your taxes jointly to qualify for subsidies.

The projection that 85% of Americans could qualify for ACA subsidies 2026 largely hinges on the continuation of the enhanced subsidies. If these enhancements are not extended beyond 2025, the eligibility landscape would revert to the pre-ARPA rules, significantly reducing the number of people who qualify and increasing costs for many.

How ACA Subsidies Are Calculated for 2026

The calculation of ACA subsidies 2026, specifically Premium Tax Credits, involves a few key steps. Understanding this process can help you estimate your potential savings.

- Determine Your Household Income and FPL: Your Modified Adjusted Gross Income (MAGI) is compared to the Federal Poverty Level (FPL) for your household size. The FPL is updated annually, so the 2026 FPL figures will be crucial.

- Identify the Benchmark Plan: The benchmark plan is the second-lowest-cost Silver plan available in your specific rating area. The cost of this plan is used as a reference point for calculating your subsidy.

- Calculate Your Contribution Cap: Under the enhanced subsidies, your contribution to the benchmark plan is capped at a certain percentage of your income, with a maximum of 8.5%. This percentage slides based on your income level. For example, lower-income individuals might be expected to pay a much smaller percentage, even 0% for those at the very lowest end of the spectrum.

- Subtract Your Contribution from Benchmark Plan Cost: The difference between the cost of the benchmark plan and your capped contribution is your Premium Tax Credit amount. This credit can then be applied to any metal-tier plan you choose, not just the Silver plan.

For example, if the benchmark plan costs $500 per month, and your income dictates that you should only pay 5% of your income for health insurance, and 5% of your income is $150, then your subsidy would be $350 ($500 – $150). This $350 could then be used to lower the premium of a Bronze, Silver, Gold, or Platinum plan.

The calculation for Cost-Sharing Reductions is simpler: if you qualify based on your income and enroll in a Silver plan, the marketplace automatically assigns you a Silver plan with enhanced benefits (e.g., lower deductible, co-pays). These reductions are applied directly to the plan’s structure.

The Impact of Enhanced Subsidies: Why 85% of Americans?

The projection that 85% of Americans could benefit from ACA subsidies 2026 is a direct consequence of the enhanced subsidies initially enacted through the American Rescue Plan Act and extended by the Inflation Reduction Act. Prior to these legislative changes, many middle-income individuals and families, particularly those earning above 400% FPL, were considered ineligible for financial assistance, leading to what was known as the ‘subsidy cliff’. They faced the full, unsubsidized cost of marketplace plans, which could be prohibitively expensive.

By eliminating the income cap and limiting premium contributions to 8.5% of household income for the benchmark plan, these enhancements made subsidies accessible to a much broader segment of the population. This not only helped lower-income individuals even further but also brought relief to middle-income households who previously struggled to afford coverage. The result is a significant increase in the number of people who find marketplace plans affordable, thus driving up the percentage of those eligible for ACA subsidies 2026.

The continued existence of these enhanced subsidies beyond 2025 is a critical policy debate. If they are allowed to expire, the 85% figure would likely drop considerably, and millions of Americans could see their health insurance premiums increase significantly. This would undoubtedly impact affordability and potentially lead to a rise in the uninsured rate. Advocates for affordable healthcare are actively pushing for the permanent extension of these enhanced subsidies, recognizing their profound impact on health access.

Navigating the Marketplace for ACA Subsidies in 2026

For those looking to take advantage of ACA subsidies 2026, the primary avenue is through the official Health Insurance Marketplace (healthcare.gov) or your state’s individual marketplace, if applicable. The enrollment process involves several key steps:

1. Gather Necessary Information

- Household Income: You’ll need an estimate of your expected household income for 2026. This includes wages, salaries, self-employment income, social security benefits, and other taxable income.

- Household Members: Information for all members of your tax household, including names, dates of birth, social security numbers, and immigration status.

- Current Health Coverage Details: If you currently have health insurance, details about your plan.

2. Create an Account and Apply

Visit healthcare.gov or your state’s marketplace website during the Open Enrollment Period (typically November 1 – January 15 for coverage starting the following year). Create an account and complete the application. The application will ask for your income and household information to determine your eligibility for ACA subsidies 2026.

3. Review Eligibility and Plan Options

Once your application is submitted, the marketplace will inform you of your eligibility for Premium Tax Credits and Cost-Sharing Reductions. You can then browse available health plans, with the subsidy amounts automatically applied to the displayed premiums. This allows for a clear comparison of net costs.

4. Choose a Plan and Enroll

Carefully compare plans based on premiums, deductibles, co-pays, out-of-pocket maximums, and network providers. Remember that if you qualify for CSRs, you must choose a Silver plan to receive those benefits. Once you’ve selected a plan, complete the enrollment process.

5. Report Life Changes

It’s crucial to report any changes to your income, household size, or eligibility for other coverage throughout the year. These changes can affect your subsidy amount. Failing to report changes could result in owing money back at tax time or receiving less assistance than you’re entitled to.

Key Considerations for ACA Subsidies in 2026

As you plan for healthcare coverage in 2026, keep the following considerations in mind regarding ACA subsidies 2026:

The Future of Enhanced Subsidies

As mentioned, the enhanced subsidies are currently scheduled to expire at the end of 2025. The political climate and legislative priorities leading up to 2026 will heavily influence whether these enhancements are extended, made permanent, or allowed to lapse. This uncertainty is a major factor for individuals and policymakers alike. Staying informed about legislative developments will be vital.

Income Estimation Accuracy

Accurately estimating your household income for 2026 is paramount. If you underestimate your income, you might receive larger subsidies than you’re eligible for, potentially leading to a repayment at tax time. Conversely, overestimating could mean you miss out on financial assistance you’re entitled to. The marketplace offers tools and guidance to help with income estimation, and it’s always advisable to use the most current information available.

Plan Selection Strategy

The availability of ACA subsidies 2026 allows for strategic plan selection. If you qualify for CSRs, a Silver plan is often the best value due to its enhanced benefits. If you don’t qualify for CSRs but receive PTCs, you might consider a Bronze plan for lower premiums (with higher out-of-pocket costs) or a Gold/Platinum plan for more comprehensive coverage (with higher premiums, but still reduced by your PTCs).

Working with Navigators and Assisters

The marketplace provides free assistance from trained navigators and assisters. These individuals can help you understand your options, determine your eligibility for ACA subsidies 2026, compare plans, and enroll. Their expertise can be invaluable, especially for those new to the marketplace or facing complex situations.

State-Specific Marketplaces

While healthcare.gov serves most states, some states operate their own marketplaces. If you live in a state with its own marketplace, you’ll need to use their website for enrollment. These state-based marketplaces often have similar rules and offer the same federal subsidies, but their specific processes and deadlines might vary slightly.

Beyond 2026: The Long-Term Outlook for ACA Subsidies

The discussion around ACA subsidies 2026 is not just about the immediate future but also about the long-term trajectory of affordable healthcare in the U.S. The success of the enhanced subsidies in expanding coverage and reducing costs has demonstrated their effectiveness. However, their temporary nature introduces an element of instability for consumers and health plans.

Policymakers face a critical choice: allow the subsidies to expire, potentially jeopardizing coverage for millions, or extend them, solidifying access to affordable healthcare for a significant portion of the population. The economic implications of either decision are substantial. Extending the subsidies would require ongoing federal funding, while allowing them to expire could lead to increased uncompensated care costs and a less healthy workforce.

The focus on ACA subsidies 2026 highlights the ongoing debate about the role of government in healthcare and the balance between individual responsibility and collective well-being. As the nation grapples with rising healthcare costs, the mechanisms for making insurance affordable, such as the ACA subsidies, will remain at the forefront of policy discussions.

Conclusion: Preparing for ACA Subsidies in 2026

The prospect of 85% of Americans being eligible for ACA subsidies 2026 offers a hopeful outlook for healthcare affordability. These subsidies, particularly the enhanced Premium Tax Credits and valuable Cost-Sharing Reductions, are powerful tools designed to ensure that health insurance is within reach for a vast majority of the population. However, the temporary nature of the enhanced subsidies means that vigilance and advocacy will be key in securing their future.

As 2026 approaches, it is essential for individuals and families to proactively understand their eligibility, accurately estimate their income, and explore the options available through the Health Insurance Marketplace. By doing so, they can maximize their financial assistance and secure comprehensive health coverage that meets their needs without imposing undue financial burden. Stay informed about legislative developments, utilize the resources available on healthcare.gov or your state’s marketplace, and don’t hesitate to seek assistance from navigators or assisters. Your health and financial well-being depend on making informed choices about ACA subsidies 2026.

The journey towards universal, affordable healthcare is complex and continuous. The current reach of ACA subsidies represents a significant step forward, offering a safety net for millions. Understanding and leveraging these subsidies in 2026 will be crucial for maintaining and further improving access to vital healthcare services across the nation.