Navigating 2026 Student Loan Interest Rate Caps and Repayment Options

Understanding the New 2026 Student Loan Interest Rate Caps and Repayment Options

The world of student loans is constantly evolving, and for those pursuing higher education or already managing their debt, understanding these changes is paramount. As we approach 2026, significant adjustments are on the horizon, particularly concerning student loan interest rate caps and the array of repayment options available. These impending changes could profoundly impact millions of borrowers, shaping their financial futures and influencing their educational and career decisions. This comprehensive guide aims to demystify the upcoming alterations, providing clarity on what to expect and how to prepare for the student loan changes 2026.

For many, student loans represent a necessary investment in their future, a gateway to opportunities that might otherwise be inaccessible. However, the burden of repayment, especially when coupled with fluctuating interest rates, can be a significant source of stress. The federal government and various financial institutions periodically review and revise their policies to address these concerns, aiming to strike a balance between supporting educational access and maintaining fiscal responsibility. The 2026 updates are a testament to this ongoing effort, introducing measures designed to offer greater predictability and potentially more manageable repayment paths for borrowers.

This article will delve into the specifics of the new interest rate caps, exploring their implications for both current and future borrowers. We will also meticulously examine the expanded and revised repayment options, including income-driven repayment plans, forbearance, deferment, and potential new initiatives. Our goal is to equip you with the knowledge needed to navigate this complex financial landscape, ensuring you can make informed decisions that align with your long-term financial goals. Understanding these changes early can provide a crucial advantage, allowing you to strategize effectively and minimize the financial strain of student loan debt.

The Rationale Behind the 2026 Student Loan Changes

Before diving into the specifics, it’s essential to understand why these student loan changes 2026 are being implemented. The overarching goal is often to create a more equitable and sustainable student loan system. High interest rates can lead to ballooning debt, making it difficult for graduates to achieve financial milestones like homeownership or starting a family. Moreover, complex repayment structures can confuse borrowers, leading to defaults or extended repayment periods. The 2026 reforms are likely a response to these systemic issues, aiming to provide a clearer, more predictable, and ultimately more borrower-friendly environment.

One of the primary drivers for capping interest rates is to mitigate the risk of excessive debt accumulation. When interest rates are high, a significant portion of a borrower’s payments goes towards interest rather than the principal, prolonging the repayment period and increasing the total cost of the loan. By setting caps, the government seeks to ensure that student loans remain a viable and affordable option for financing education, preventing situations where the cost of borrowing overshadows the benefits of the degree itself.

Furthermore, the expansion and refinement of repayment options reflect a recognition that a one-size-fits-all approach does not work for all borrowers. Life circumstances can change dramatically, impacting one’s ability to make consistent loan payments. Income-driven repayment (IDR) plans, for instance, are designed to adjust monthly payments based on a borrower’s income and family size, offering a crucial safety net during periods of financial hardship. The 2026 changes could introduce more flexible IDR plans, make existing ones more accessible, or even introduce new mechanisms to help borrowers manage their debt more effectively. These adjustments are critical for promoting financial stability and reducing the incidence of loan defaults, which have broader economic implications.

Another factor influencing these changes is the ongoing debate about the value of higher education and its accessibility. As tuition costs continue to rise, student loans play an increasingly vital role. Policymakers are constantly evaluating how to balance the need for accessible education with the imperative of responsible lending. The 2026 reforms are part of this continuous dialogue, seeking to optimize the system for both borrowers and taxpayers. Understanding this broader context can help you appreciate the significance of the upcoming changes and how they fit into the larger landscape of educational finance.

The New Interest Rate Caps for 2026

Perhaps the most anticipated aspect of the student loan changes 2026 is the introduction or revision of interest rate caps. While the exact figures will depend on final legislative decisions and economic forecasts, the principle behind these caps is clear: to limit the maximum interest rate that can be charged on federal student loans. This move is designed to provide borrowers with greater certainty and protection against excessively high interest accrual.

Historically, federal student loan interest rates have been fixed for the life of the loan, determined by a formula that often involves the 10-year Treasury note auction results. While this provides stability, it doesn’t always protect borrowers from market fluctuations that could lead to higher initial rates. The new caps are expected to introduce an upper limit, ensuring that even in periods of rising interest rates, student borrowers will not face exorbitant charges. This is particularly beneficial for students taking out loans in periods of economic uncertainty or high inflation.

Impact on Different Loan Types

- Direct Subsidized Loans: These loans are typically offered to undergraduate students with demonstrated financial need. The government pays the interest while the student is in school at least half-time, during the grace period, and during deferment. Any interest rate caps here would further enhance their affordability.

- Direct Unsubsidized Loans: Available to undergraduate and graduate students regardless of financial need, interest accrues on these loans from the moment they are disbursed. A cap on these rates would be highly beneficial for all borrowers, especially graduate students who often take on larger loan amounts.

- Direct PLUS Loans (Parent PLUS and Grad PLUS): These loans typically have higher interest rates than subsidized or unsubsidized loans. An interest rate cap on PLUS loans would be a significant relief for parents and graduate students, potentially saving them thousands of dollars over the life of the loan.

It is crucial for prospective and current borrowers to monitor official announcements from the Department of Education or their loan servicers regarding the precise percentages of these caps. These figures will directly influence the total cost of their education and their long-term repayment strategies. Understanding the maximum rate you could be charged allows for more accurate financial planning and budgeting, reducing the element of surprise when repayment begins. Moreover, these caps might encourage more students to pursue higher education, knowing that the cost of borrowing is somewhat contained.

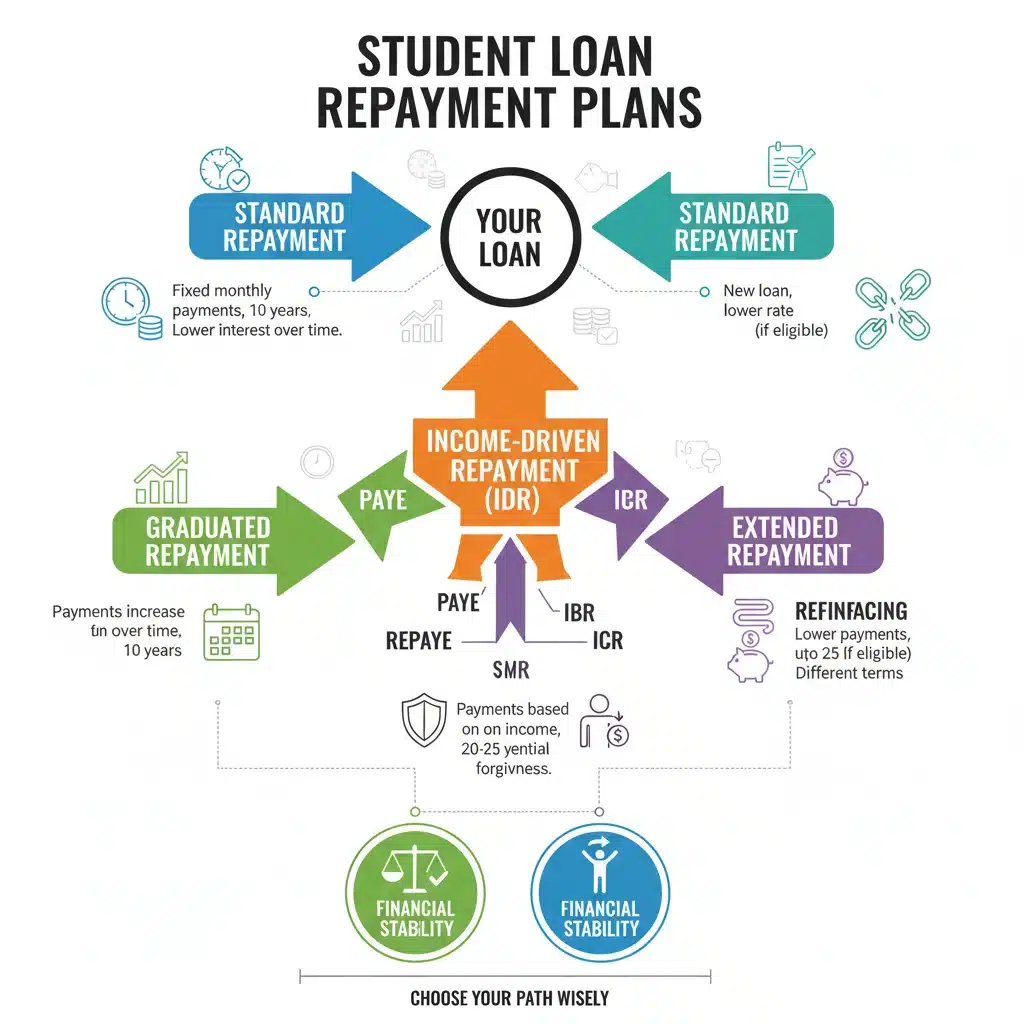

Expanded and Revised Repayment Options for 2026

Beyond interest rate caps, the student loan changes 2026 are also expected to bring significant enhancements to repayment options. These changes are designed to offer greater flexibility, reduce monthly burdens, and provide clearer pathways to loan forgiveness for eligible borrowers. The goal is to make student loan repayment less daunting and more manageable, adapting to the diverse financial realities of graduates.

Key Repayment Plan Revisions to Anticipate:

- Income-Driven Repayment (IDR) Plans: These plans adjust your monthly payment based on your income and family size. The 2026 changes could make IDR plans more generous, potentially by reducing the percentage of discretionary income used to calculate payments, expanding eligibility, or simplifying the application and recertification process. This would make these plans a more effective safety net for borrowers experiencing financial hardship.

- Public Service Loan Forgiveness (PSLF): While not a direct repayment plan, PSLF is a critical program for those working in public service. The 2026 reforms might include streamlining PSLF requirements, making it easier for eligible borrowers to track their payments and ultimately achieve forgiveness. There could also be broader definitions of what constitutes ‘public service’ or ‘eligible payments’.

- Simplified Repayment Plan Selection: The current array of repayment plans can be confusing. The 2026 changes might introduce a more streamlined process for selecting the most appropriate plan, perhaps through enhanced online tools or personalized guidance from loan servicers. This would reduce borrower confusion and ensure more individuals are enrolled in plans that best suit their financial situation.

- New Forbearance and Deferment Policies: These options allow borrowers to temporarily pause or reduce their loan payments under specific circumstances. The 2026 updates could expand the qualifying conditions for forbearance and deferment, or extend the maximum duration for these periods, offering greater relief during unforeseen financial challenges or career transitions.

These revisions underscore a commitment to making student loan repayment more adaptable to individual circumstances. For borrowers struggling with high monthly payments, the enhanced IDR options could be a lifeline, preventing defaults and improving credit scores. For those dedicated to public service, a clearer path to PSLF could incentivize them to continue their valuable work without the overwhelming burden of student debt. Staying informed about these specific changes as they are finalized will be crucial for all borrowers.

Who Will Be Affected by the 2026 Changes?

The student loan changes 2026 are broad in scope and will likely impact a wide range of individuals connected to the higher education system. Understanding who stands to gain or be affected most is key to preparing for the future.

Current Students

Students currently enrolled in undergraduate or graduate programs will be directly affected, especially if they are taking out new federal loans after the changes come into effect. The new interest rate caps could mean lower overall borrowing costs for their remaining years of study. Furthermore, understanding the revised repayment options before graduation can help them plan their post-college finances more effectively. They should pay close attention to how these changes might influence their future monthly payments and eligibility for various forgiveness programs.

Future Students and Their Families

Prospective students and their families will also feel the impact. The promise of lower interest rate caps and more flexible repayment plans might make higher education seem more accessible and less financially daunting. This could influence decisions about which institutions to attend, what fields of study to pursue, and even whether to pursue higher education at all. Parents considering PLUS loans for their children will also benefit from potentially lower interest rates and clearer repayment pathways.

Current Borrowers in Repayment

Existing borrowers who are already in repayment might also see benefits, particularly regarding the expanded repayment options. If new, more generous IDR plans are introduced, they might be able to switch to a plan that offers lower monthly payments or a faster path to forgiveness. However, it’s important to note that changes to interest rates typically only apply to new loans disbursed after the effective date of the change. Existing loan interest rates are usually fixed. Still, the repayment option enhancements are likely to be available to all eligible federal loan borrowers.

Loan Servicers

Student loan servicers will also be significantly affected as they will need to implement the new policies, update their systems, and educate borrowers about the revised terms. This could lead to temporary adjustments in their operations as they adapt to the new regulatory environment.

Staying abreast of these changes is not just about compliance; it’s about optimizing your financial strategy. Whether you’re a student, a parent, or a graduate already in repayment, the 2026 changes offer an opportunity to re-evaluate your student loan strategy and ensure it aligns with your financial well-being.

Preparing for the 2026 Student Loan Changes

Proactive preparation is crucial to maximize the benefits and mitigate any potential challenges arising from the student loan changes 2026. Here are actionable steps you can take:

1. Stay Informed Through Official Channels

The most reliable information will come from the U.S. Department of Education, your loan servicer, and reputable financial aid organizations. Regularly check their websites for updates. Avoid relying solely on unofficial sources, as misinformation can lead to poor financial decisions. Sign up for newsletters and alerts from these official bodies to receive timely notifications.

2. Review Your Current Loan Portfolio

Familiarize yourself with your existing federal student loans. Understand your current interest rates, loan types (subsidized, unsubsidized, PLUS), and your current repayment plan. This knowledge will be invaluable when assessing how the new policies might affect you. Log into your account on the Federal Student Aid website (StudentAid.gov) to access your loan history and details.

3. Understand the Specifics of Interest Rate Caps

Once the final interest rate caps are announced, compare them to your current or anticipated loan rates. If you are a prospective borrower, factor these caps into your borrowing decisions. For current borrowers, remember that these caps typically apply to new loans, but understanding them can still inform future financial planning and refinancing considerations.

4. Evaluate New Repayment Options

As the details of expanded and revised repayment options become available, carefully assess how they could benefit you. If you’re currently on a standard repayment plan, an updated income-driven repayment plan might offer lower monthly payments. If you’re pursuing public service, track any changes to PSLF requirements closely. Use online calculators and speak with your loan servicer to model different scenarios.

5. Update Your Contact Information

Ensure your loan servicer and the Federal Student Aid office have your most current contact information (email, phone, mailing address). This will ensure you receive important communications about the changes and any required actions on your part.

6. Seek Professional Financial Advice

If you have a complex loan situation or are unsure how the changes will impact your personal finances, consider consulting with a financial advisor specializing in student loan debt. They can provide personalized guidance and help you develop a tailored strategy. Non-profit credit counseling agencies can also offer valuable, often free, advice.

7. Budget and Plan Ahead

Regardless of the changes, maintaining a robust personal budget is always wise. If you anticipate lower payments due to new IDR options, consider using the extra funds to build an emergency savings fund or pay down other high-interest debt. If you’re a future student, budget for your educational expenses with the new interest rate caps in mind.

Long-Term Implications of the 2026 Changes

The student loan changes 2026 are not just about immediate relief; they carry significant long-term implications for individuals and the broader economy. These reforms could reshape how Americans perceive and manage educational debt for decades to come.

For Individual Borrowers

For individual borrowers, the long-term impact could be profound. Lower interest rate caps mean a reduced total cost of borrowing, freeing up more disposable income over the life of the loan. This can accelerate financial milestones such as saving for a down payment on a home, investing for retirement, or starting a business. More flexible repayment options, particularly enhanced IDR plans, can provide greater financial stability, reducing the stress associated with student debt and improving overall credit health by preventing defaults.

The clearer pathways to loan forgiveness, especially for those in public service, can also incentivize career choices that benefit society while providing a tangible financial reward. This could lead to a more diverse workforce in critical sectors that traditionally suffer from high turnover due to low pay relative to student debt burdens.

For Higher Education Institutions

Higher education institutions might also see shifts. With potentially more affordable borrowing, the demand for higher education could increase, particularly for programs that were previously deemed too expensive. However, institutions might also face pressure to justify tuition costs if the government is taking on more risk through lower interest rates and generous repayment plans. This could lead to a renewed focus on cost-efficiency and value proposition in higher education.

For the Economy

On a macro-economic level, the changes could stimulate economic growth. When borrowers have less student loan debt, they have more money to spend, save, and invest. This increased consumer spending and investment can boost various sectors of the economy. Reduced default rates also strengthen the financial system. However, there will also be a cost associated with these changes, likely borne by taxpayers, which will be a subject of ongoing debate and fiscal management.

Addressing Educational Access and Equity

Ultimately, these reforms are part of a larger conversation about educational access and equity. By making student loans more manageable, the government aims to ensure that financial barriers do not unduly prevent individuals from pursuing higher education and achieving their full potential. The 2026 changes represent a significant step in this ongoing effort, aiming to create a more supportive and sustainable environment for students and graduates alike.

Conclusion: A New Era for Student Loan Management

The upcoming student loan changes 2026 mark a pivotal moment in the landscape of higher education finance. With new interest rate caps and potentially expanded and more flexible repayment options, borrowers are poised to enter an era of greater predictability and support in managing their educational debt. These reforms reflect a broader commitment to ensuring that student loans remain a tool for opportunity, rather than an insurmountable burden.

While the precise details are still being finalized and will require diligent monitoring, the direction of these changes is clear: towards a more borrower-friendly system. For current and prospective students, these adjustments could mean a more affordable path to their academic and career aspirations. For graduates already in repayment, the revisions to income-driven plans and forgiveness programs could offer much-needed relief and a clearer horizon.

The key to navigating these changes successfully lies in proactive engagement. Staying informed through official sources, thoroughly reviewing your personal loan situation, and understanding how the new policies apply to you are paramount. Don’t hesitate to leverage the resources available, whether it’s your loan servicer, the Federal Student Aid website, or a trusted financial advisor. Building a robust financial plan that incorporates these new realities will empower you to manage your student loans effectively, paving the way for a more secure financial future.

As 2026 approaches, the focus for millions will shift to understanding and adapting to these new rules. By taking the time to educate yourself and plan accordingly, you can ensure that you are well-positioned to benefit from these significant reforms and continue on your path to financial success and educational fulfillment.