Cut Capital Gains Tax 2026: Expert Strategies to Reduce Your Exposure by 15%

As 2026 approaches, investors are increasingly looking for effective ways to reduce capital gains tax exposure. The landscape of tax laws is constantly evolving, making proactive and informed planning more crucial than ever. For many, the goal isn’t just to minimize taxes, but to do so strategically, ensuring that wealth accumulation and financial objectives remain on track. This comprehensive guide will delve into expert strategies designed to help you significantly reduce your capital gains tax burden, potentially by 15% or more, by leveraging legitimate and powerful tax planning tools.

Capital gains tax can be a significant drag on investment returns. Whether you’ve profited from selling stocks, real estate, or other appreciated assets, understanding how to manage this tax is paramount to optimizing your financial health. This article will equip you with the knowledge and actionable steps needed to navigate the complexities of capital gains taxation, focusing on strategies that are particularly relevant for the 2026 tax year.

The journey to effectively reduce capital gains begins with a thorough understanding of what they are and how they are calculated. Simply put, a capital gain occurs when you sell an asset for more than its purchase price. The tax rate applied to these gains depends on several factors, including your income level and how long you held the asset. Short-term capital gains (assets held for one year or less) are typically taxed at your ordinary income tax rate, which can be as high as 37%. Long-term capital gains (assets held for more than one year) usually benefit from lower, preferential tax rates, currently 0%, 15%, or 20%, depending on your taxable income.

Our focus here will be on strategies applicable to both short-term and long-term gains, with an emphasis on long-term gains due to their prevalence in investment portfolios. By implementing the techniques discussed, you can not only reduce your immediate tax liability but also foster a more tax-efficient investment approach for the future. Let’s explore the key strategies that can help you achieve your goal of substantial capital gains tax reduction.

Understanding the Basics of Capital Gains Tax for 2026

Before diving into advanced strategies, it’s essential to solidify your understanding of capital gains tax. For the 2026 tax year, while specific rates are subject to congressional changes, the general framework is expected to remain similar to current law. This means distinguishing between short-term and long-term gains will continue to be a critical factor in determining your tax liability.

Short-Term vs. Long-Term Capital Gains

As mentioned, the holding period of an asset is crucial. If you sell an asset after holding it for one year or less, any profit is considered a short-term capital gain. These gains are added to your ordinary income and taxed at your marginal income tax rate. This can be particularly punitive for high-income earners. Conversely, if you hold an asset for more than one year before selling, the profit is a long-term capital gain, subject to more favorable rates.

Net Investment Income Tax (NIIT)

For high-income individuals, an additional tax layer comes into play: the 3.8% Net Investment Income Tax (NIIT). This tax applies to the lesser of your net investment income or the amount by which your modified adjusted gross income (MAGI) exceeds certain thresholds (e.g., $200,000 for single filers, $250,000 for married filing jointly). Capital gains are typically included in net investment income, so strategies to reduce capital gains can also help mitigate your NIIT exposure.

State Capital Gains Taxes

It’s also important to remember that federal capital gains taxes are only part of the equation. Most states also impose their own income taxes, which often include capital gains. These state taxes can vary widely, from zero in states like Florida and Texas to significant percentages in others like California and New York. When planning to reduce capital gains, consider the combined federal and state tax burden.

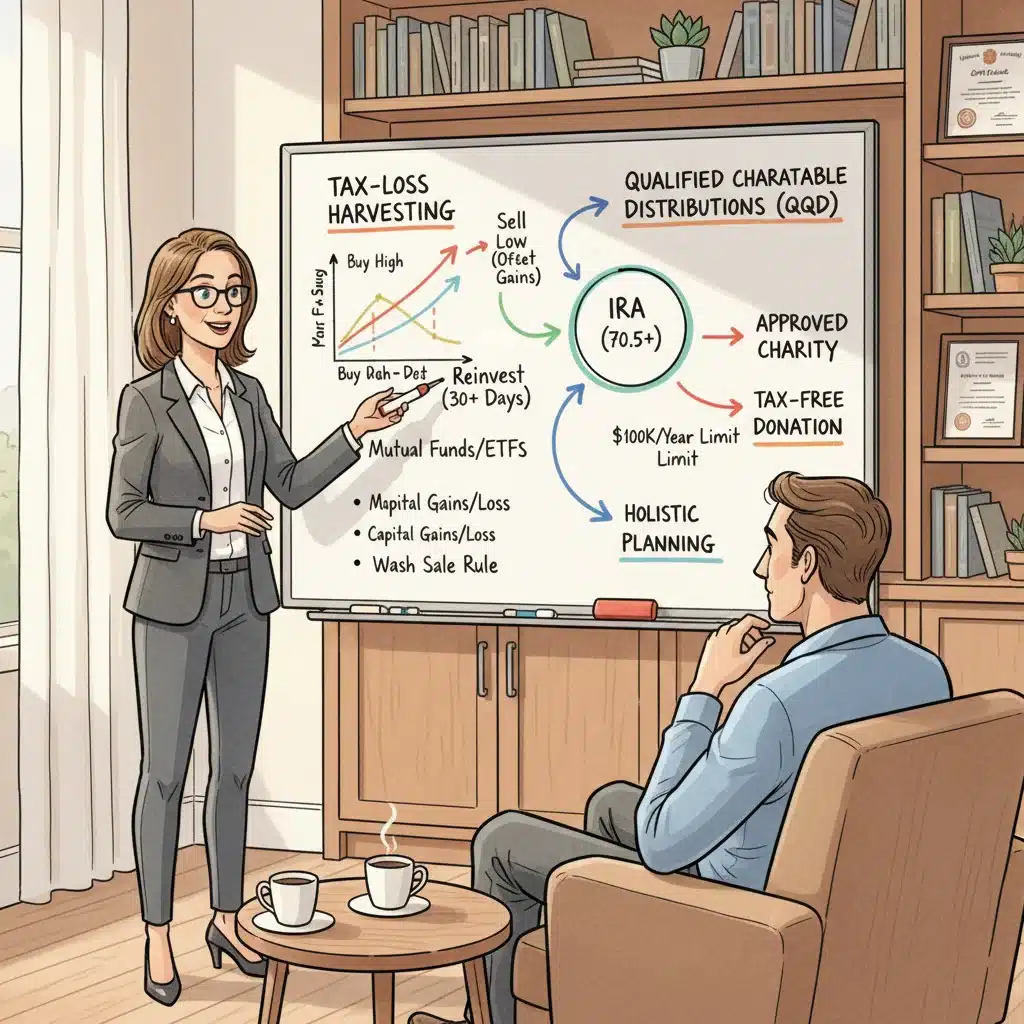

Strategic Tax-Loss Harvesting: A Cornerstone for Capital Gains Reduction

One of the most powerful and widely used strategies to reduce capital gains is tax-loss harvesting. This involves strategically selling investments at a loss to offset capital gains and, potentially, a limited amount of ordinary income.

How Tax-Loss Harvesting Works

The core principle is simple: if you have realized capital gains from selling profitable investments, you can sell other investments that have declined in value to generate capital losses. These losses can then be used to offset your capital gains dollar for dollar. For example, if you have $10,000 in capital gains from selling stock A, and you sell stock B for a $10,000 loss, your net capital gain for the year becomes zero, effectively eliminating the tax on those gains.

If your capital losses exceed your capital gains, you can use up to $3,000 of the remaining loss to offset ordinary income each year. Any unused losses can be carried forward indefinitely to offset future capital gains and ordinary income. This carryover feature makes tax-loss harvesting a long-term strategy for managing your tax liability.

Best Practices for Tax-Loss Harvesting

- Timing is Key: While often done at year-end, tax-loss harvesting can be performed throughout the year. Monitoring your portfolio for opportunities to realize losses can be beneficial.

- The Wash-Sale Rule: Be acutely aware of the wash-sale rule. This IRS rule prohibits you from claiming a loss on a security if you buy a substantially identical security within 30 days before or after the sale. Violating this rule will disallow the loss.

- Reinvestment Strategy: If you want to maintain your market exposure, you can sell the losing security and immediately reinvest the proceeds into a different, but similar, security (e.g., an ETF that tracks the same sector but is not ‘substantially identical’). After 31 days, you can repurchase the original security if you wish.

- Long-Term vs. Short-Term Losses: Capital losses are first used to offset capital gains of the same type (short-term losses against short-term gains, long-term losses against long-term gains). If there’s an excess, they can then be used against the other type of gain. This distinction matters because short-term gains are taxed at higher rates.

Implementing a consistent tax-loss harvesting strategy can significantly reduce capital gains, especially in volatile markets where investment losses are more common. It’s a proactive approach that turns market downturns into tax advantages.

Leveraging Charitable Contributions to Reduce Capital Gains

For philanthropically inclined investors, charitable giving offers a dual benefit: supporting causes you care about and potentially reducing your capital gains tax burden. The key is in how you structure these donations.

Donating Appreciated Securities

Instead of donating cash, consider donating appreciated securities that you’ve held for more than a year. When you donate appreciated stock directly to a qualified charity, you can typically deduct the fair market value of the stock on the date of the donation, subject to certain AGI limitations. Even better, you avoid paying capital gains tax on the appreciation of the stock. The charity, being tax-exempt, also won’t pay capital gains tax when they sell the stock.

For example, if you bought stock for $1,000 and it’s now worth $10,000, donating it directly to charity allows you to claim a $10,000 deduction (if you itemize) and avoid paying capital gains tax on the $9,000 appreciation. If you had sold the stock first, you would have paid capital gains tax on the $9,000 profit, reducing the amount you could donate and your overall tax benefit.

Qualified Charitable Distributions (QCDs)

For individuals aged 70½ or older, Qualified Charitable Distributions (QCDs) from an IRA are an excellent way to reduce capital gains and satisfy Required Minimum Distributions (RMDs). You can distribute up to $100,000 directly from your IRA to a qualified charity each year. While a QCD isn’t deductible as a charitable contribution, it reduces your adjusted gross income (AGI) because the distribution isn’t included in your taxable income. This lower AGI can have a ripple effect, potentially reducing your Medicare premiums and keeping you below thresholds for other taxes, including the NIIT.

Donor-Advised Funds (DAFs)

Donor-advised funds (DAFs) offer another flexible and tax-efficient way to give. You can contribute appreciated assets to a DAF, receive an immediate tax deduction for the full market value, and avoid capital gains tax on the donated assets. You then recommend grants from the DAF to your favorite charities over time. This allows you to claim a large deduction in the year of contribution, even if you spread out your charitable giving over many years.

By strategically incorporating charitable giving into your financial plan, you can effectively reduce capital gains while making a positive impact on society.

Exploring Tax-Advantaged Investment Vehicles and Strategies

Beyond harvesting losses and charitable giving, several investment vehicles and strategies are inherently designed to be tax-efficient, helping you reduce capital gains over the long term.

Opportunity Zones (OZs)

Opportunity Zones are economically distressed communities where new investments, under certain conditions, are eligible for preferential tax treatment. Investing capital gains into a Qualified Opportunity Fund (QOF) offers three significant tax benefits:

- Deferral: You can defer capital gains tax on the original gain until the earlier of December 31, 2026, or when you sell your QOF investment.

- Reduction: If you hold your QOF investment for at least five years, your deferred capital gains tax basis increases by 10%. If held for seven years, it increases by an additional 5%, totaling a 15% exclusion of the original gain. This is directly aligned with our goal to reduce capital gains by 15% for 2026.

- Exclusion: If you hold your QOF investment for at least ten years, you pay no capital gains tax on any appreciation of the QOF investment itself.

Opportunity Zones present a powerful, albeit complex, strategy for investors with significant capital gains, particularly those looking for long-term investments in real estate or businesses within designated zones.

Tax-Advantaged Retirement Accounts

Maxing out contributions to tax-advantaged retirement accounts like 401(k)s and IRAs is a fundamental strategy for tax deferral. While these don’t directly reduce capital gains on taxable investments, they allow your investments within these accounts to grow tax-deferred (Traditional accounts) or tax-free (Roth accounts). This means you won’t pay capital gains tax year-to-year on trades within these accounts, effectively postponing or eliminating the tax burden until withdrawal (Traditional) or forever (Roth).

Municipal Bonds

Interest earned on municipal bonds is generally exempt from federal income tax and, often, from state and local taxes if you reside in the issuing state. While municipal bonds don’t directly deal with capital gains, they offer tax-free income, which can reduce your overall taxable income and potentially keep you in a lower tax bracket for capital gains purposes.

Long-Term Holding Periods

This is perhaps the simplest strategy: hold your investments for more than one year. By doing so, any gains realized will be treated as long-term capital gains, subject to the lower preferential tax rates (0%, 15%, or 20%) rather than your higher ordinary income tax rates. Patient investing is not just good for returns; it’s excellent for tax efficiency. This foundational approach is key to significantly reducing your overall capital gains tax burden.

Advanced Planning Techniques for Significant Capital Gains

For those with substantial wealth and complex financial situations, more advanced planning techniques can be employed to reduce capital gains, often requiring the expertise of a financial advisor or tax professional.

Installment Sales

If you sell a property or business and receive payments over several years, you might be able to use an installment sale. This allows you to defer the recognition of capital gains until you receive the payments, spreading the tax liability over multiple tax years. This can be particularly useful if recognizing the entire gain in one year would push you into a higher tax bracket or trigger the NIIT.

Qualified Small Business Stock (QSBS) Exclusion

If you invest in qualified small business stock (QSBS) and meet specific criteria, you might be able to exclude a significant portion, or even all, of the capital gains when you sell the stock. This exclusion can be up to $10 million or 10 times the adjusted basis of the stock, whichever is greater. To qualify, the stock must be issued by a C corporation with gross assets of $50 million or less at the time of issuance, and you must hold the stock for more than five years. This is a powerful, though specialized, way to reduce capital gains for entrepreneurs and early-stage investors.

Exchange Funds (Partnership Swaps)

For investors with highly appreciated, concentrated stock positions, an exchange fund (also known as a partnership swap) can offer a way to diversify a portfolio without triggering immediate capital gains tax. You contribute your appreciated stock to a partnership in exchange for an interest in a diversified portfolio of securities. While complex and with specific rules, this allows for diversification on a tax-deferred basis.

Charitable Remainder Trusts (CRTs)

A Charitable Remainder Trust (CRT) allows you to donate appreciated assets to a trust, receive an income stream for a specified period (or for life), and then have the remaining assets go to charity. When you transfer appreciated assets into a CRT, you avoid paying capital gains tax on the transfer. The trust can then sell the assets tax-free. You receive a partial income tax deduction in the year of contribution, and the income stream you receive from the trust is taxable, but often spread out over many years, potentially at lower rates. This is an excellent strategy for those looking to generate income, reduce capital gains, and leave a legacy.

Common Pitfalls to Avoid When Trying to Reduce Capital Gains

While the strategies discussed can be highly effective, it’s equally important to be aware of common mistakes that can undermine your efforts to reduce capital gains.

Ignoring the Wash-Sale Rule

As mentioned earlier, the wash-sale rule is a frequent trap. Selling a security at a loss and then repurchasing the same or a ‘substantially identical’ security within 30 days will disallow the loss. Ensure you understand and abide by this rule when tax-loss harvesting.

Failing to Track Basis Accurately

Maintaining accurate records of your cost basis (original purchase price plus commissions, minus returns, etc.) for all investments is critical. Without proper basis tracking, you might overstate your gains or understate your losses, leading to incorrect tax calculations and potential issues with the IRS. Many brokerage firms provide this information, but it’s wise to double-check.

Not Considering State Taxes

Focusing solely on federal capital gains taxes can lead to an incomplete picture. State income and capital gains taxes can add a significant layer to your overall tax burden. Always consider the combined federal and state impact of your tax planning strategies.

Making Emotional Investment Decisions

Tax strategies should complement, not dictate, your investment decisions. Selling a winning stock prematurely just to avoid long-term capital gains, or holding onto a losing stock longer than prudent for tax-loss harvesting, can be counterproductive to your overall financial goals. Always prioritize sound investment principles.

Delaying Tax Planning

Procrastination is the enemy of effective tax planning. Many of the most powerful strategies, such as investing in Opportunity Zones or establishing a CRT, require significant lead time and careful execution. Waiting until the end of the year often limits your options to reduce capital gains.

Working with a Financial Advisor for Optimal Capital Gains Management

Given the complexity of tax laws and the myriad of strategies available, working with a qualified financial advisor or tax professional is often the best approach to effectively reduce capital gains. An expert can provide personalized guidance tailored to your specific financial situation, investment portfolio, and long-term goals.

Benefits of Professional Guidance

- Personalized Strategy: A professional can help you identify which strategies are most relevant and beneficial for your unique circumstances.

- Compliance: They ensure that all your tax planning activities comply with current IRS regulations, minimizing the risk of audits or penalties.

- Holistic Planning: Tax planning doesn’t exist in a vacuum. A good advisor integrates capital gains strategies with your broader financial plan, including retirement planning, estate planning, and wealth management.

- Staying Current: Tax laws frequently change. A professional stays updated on new legislation and can adapt your strategies accordingly for 2026 and beyond.

- Maximizing Benefits: They can help you optimize the timing and execution of various strategies to maximize your tax savings.

When seeking an advisor, look for someone with experience in tax planning, a strong fiduciary duty, and transparent fee structures. Their expertise can be invaluable in helping you achieve your goal to significantly reduce capital gains.

Conclusion: Proactive Steps to Reduce Capital Gains in 2026

Reducing your capital gains tax exposure by 15% or more in 2026 is an achievable goal with diligent planning and strategic execution. From fundamental practices like tax-loss harvesting and holding investments long-term to more advanced techniques such as Qualified Opportunity Funds and Charitable Remainder Trusts, a diverse toolkit is available to investors. The key to success lies in understanding these strategies, planning proactively, and ideally, collaborating with experienced financial and tax professionals.

Remember, every investment decision has tax implications. By integrating tax efficiency into your overall investment philosophy, you can not only minimize your tax burden but also accelerate your wealth accumulation. Start reviewing your portfolio and financial plan today to identify opportunities to reduce capital gains for the upcoming tax year. The time and effort invested now will pay significant dividends in the future, allowing you to retain more of your hard-earned investment returns.

Stay informed, stay proactive, and make 2026 a year of optimized tax efficiency for your investment portfolio. The strategies outlined in this guide provide a robust framework for achieving your capital gains reduction goals, ensuring your financial future is as bright as possible.

for Growth & Tax Benefits")