Safeguarding Retirement: Navigating 3.5% Inflation in 2026

Understanding the Impact of 3.5% Inflation on Your Retirement Savings in Early 2026: Strategies for Preservation

As we approach early 2026, the prospect of a 3.5% inflation rate looms large over the financial landscape, particularly for those in or nearing retirement. While 3.5% might not sound alarmingly high to some, its persistent erosion of purchasing power can significantly impact your carefully accumulated retirement savings over time. This comprehensive guide will delve into what 3.5% inflation retirement implications mean for your financial future and, more importantly, equip you with actionable strategies to preserve and even grow your wealth.

Retirement planning is often viewed through the lens of accumulation – saving diligently, investing wisely, and watching your nest egg grow. However, a crucial, yet frequently underestimated, adversary to this growth is inflation. Inflation, simply put, is the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your investments aren’t generating returns that outpace inflation, your money is effectively losing value, even if the nominal amount appears to stay the same or increase slightly.

The Silent Thief: How 3.5% Inflation Erodes Retirement Savings

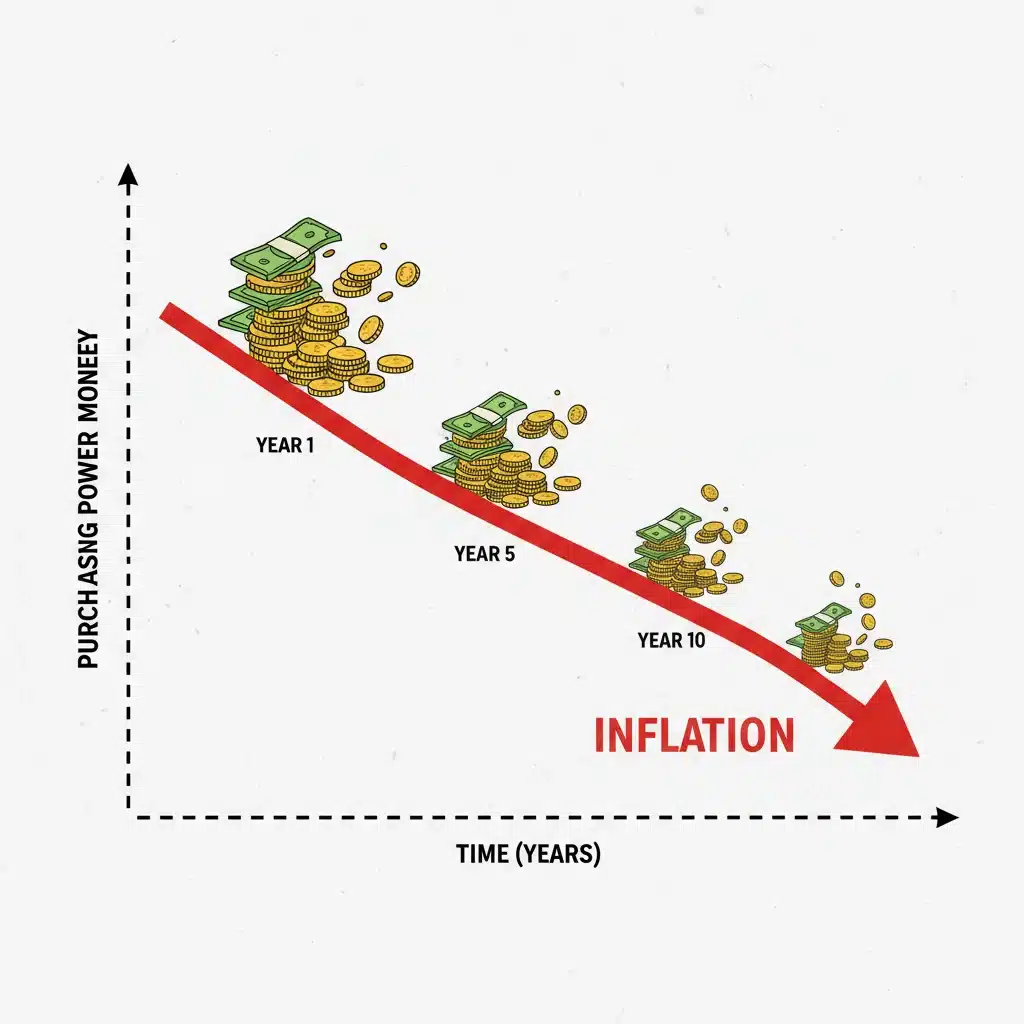

Imagine you have a retirement fund of $1,000,000. If the inflation rate is a consistent 3.5% per year, the purchasing power of that million dollars will diminish considerably over time. After just one year, what cost $1,000,000 today will cost approximately $1,035,000. This might seem manageable, but compound inflation truly reveals its power over decades. For a retiree living on a fixed income, this means that their expenses will steadily climb, while their income may not keep pace, leading to a noticeable reduction in their quality of life.

Consider the cost of everyday necessities: groceries, utilities, healthcare, and transportation. These are not discretionary expenses; they are fundamental to daily living. A 3.5% annual increase in these costs means that your fixed retirement income will buy less and less each year. Over a 20- or 30-year retirement, this seemingly modest inflation rate can halve the real value of your savings. This is why understanding and actively combating the effects of 3.5% inflation retirement planning is paramount.

Moreover, the impact extends beyond just everyday expenses. Healthcare costs, for instance, have historically outpaced general inflation. For retirees, who typically have higher healthcare needs, this can be a double whammy. Long-term care, prescription drugs, and medical procedures can become significantly more expensive, eating into savings at an accelerated rate if not properly accounted for.

Analyzing the Early 2026 Economic Landscape and Inflation Drivers

To effectively plan for 3.5% inflation retirement strategies, it’s crucial to understand the potential drivers behind this forecast. While economic predictions are never absolute, several factors could contribute to sustained inflation in early 2026:

- Supply Chain Disruptions: Lingering effects from global events, geopolitical tensions, or new challenges could continue to disrupt supply chains, driving up the cost of goods due to scarcity and increased transportation expenses.

- Strong Consumer Demand: Robust economic growth and accumulated savings could fuel strong consumer demand, allowing businesses to raise prices without fear of losing customers.

- Wage Growth: A tight labor market and increased labor union activity could lead to sustained wage growth. While beneficial for workers, higher labor costs are often passed on to consumers through higher prices.

- Fiscal Policy: Government spending and budgetary policies can inject liquidity into the economy, potentially stimulating demand and contributing to inflationary pressures.

- Monetary Policy: The stance of central banks on interest rates and quantitative easing/tightening will play a significant role. If monetary policy is perceived as too accommodative, it could fuel inflation.

- Energy Prices: Fluctuations in global energy markets (oil, natural gas) can have a cascading effect across the economy, impacting production, transportation, and consumer costs.

Understanding these potential drivers allows for a more nuanced approach to investment and financial planning, enabling you to anticipate and react to changes that might exacerbate or mitigate the impact of inflation.

Traditional Retirement Planning vs. Inflation-Adjusted Planning

Many traditional retirement planning models often assume a low, stable inflation rate, or even neglect it entirely in early calculations. This oversight can be catastrophic. An inflation-adjusted retirement plan, however, explicitly factors in the erosion of purchasing power. It asks not just ‘How much money will I have?’, but ‘What will that money buy in the future?’

For example, if you aim to maintain a lifestyle that costs $50,000 per year today, with a 3.5% inflation rate, you’ll need significantly more than $50,000 in nominal terms in the future to maintain the same purchasing power. After 10 years, that $50,000 will need to be $70,530 to afford the same goods and services. After 20 years, it’s $99,489. This stark reality underscores the urgency of proactive planning against 3.5% inflation retirement scenarios.

The key difference lies in targeting a real return on your investments – a return that exceeds the inflation rate. If your portfolio grows at 6% annually while inflation is 3.5%, your real return is 2.5%. This positive real return is what truly increases your purchasing power over time. Without it, even seemingly healthy nominal gains can leave you poorer in real terms.

Proactive Strategies to Combat 3.5% Inflation in Retirement

Preserving your retirement savings against 3.5% inflation retirement challenges requires a multi-faceted approach. Here are several key strategies to consider:

1. Re-evaluate Your Investment Portfolio for Inflation Protection

Your investment strategy needs to be dynamic, adapting to the economic climate. In an inflationary environment, certain asset classes tend to perform better than others:

- Inflation-Protected Securities (TIPS): Treasury Inflation-Protected Securities (TIPS) are bonds issued by the U.S. Treasury that are indexed to inflation. Their principal value adjusts with the Consumer Price Index (CPI), making them a direct hedge against inflation. While their nominal returns might be lower, their real returns are protected.

- Real Estate: Historically, real estate has been a good hedge against inflation. Property values and rental income tend to rise with inflation, providing a tangible asset that retains its value. This can include direct ownership, Real Estate Investment Trusts (REITs), or private real estate funds.

- Commodities: Raw materials like gold, silver, oil, and agricultural products often see their prices rise during inflationary periods. Investing in commodity funds or ETFs can offer a degree of protection, though they can be volatile.

- Stocks of Companies with Pricing Power: Look for companies that have strong brands, essential products, or dominant market positions, allowing them to pass on increased costs to consumers without significant loss of sales. These often include consumer staples, healthcare, and certain technology companies.

- Dividend-Paying Stocks: Companies that consistently pay and grow their dividends can provide a rising income stream that helps offset inflation, especially if their underlying earnings also grow.

It’s crucial to diversify your portfolio across these asset classes to mitigate risk and maximize your chances of outpacing inflation. A financial advisor can help you tailor a portfolio that aligns with your risk tolerance and retirement timeline.

2. Optimize Your Income Streams

For retirees, income stability is paramount. In an inflationary environment, seeking income streams that adjust for inflation is highly beneficial:

- Social Security: Social Security benefits typically include a Cost-of-Living Adjustment (COLA) that helps them keep pace with inflation. Maximize your Social Security benefits by delaying claiming if possible, up to age 70, to receive higher payments.

- Annuities with Inflation Riders: Some annuities offer riders that provide for increasing payments over time to help combat inflation. While these often come at a higher cost, they can provide peace of mind.

- Part-time Work or Consulting: Continuing to work part-time, even for a few hours a week, can provide additional income that can be adjusted for inflation, reducing the strain on your retirement savings. This also offers social and mental benefits.

- Rental Income: If you own rental properties, periodically adjusting rental rates to reflect market conditions and inflation can provide an inflation-protected income stream.

3. Budgeting and Expense Management

Even with robust investment strategies, careful budgeting and expense management remain vital. In a 3.5% inflation retirement scenario, every dollar saved on expenses is a dollar that doesn’t need to be generated by your investments to maintain purchasing power.

- Track Your Spending: Understand exactly where your money is going. This awareness is the first step to identifying areas for potential savings.

- Prioritize Needs vs. Wants: Differentiate between essential expenses and discretionary spending. In inflationary times, you might need to make adjustments to your lifestyle.

- Shop Smart: Look for deals, buy in bulk when appropriate, and consider store brands.

- Review Subscriptions and Services: Cancel unused subscriptions and negotiate better rates for services like internet, cable, and insurance.

- Healthcare Planning: This is arguably the most critical expense for retirees. Explore Medicare Advantage plans, Medigap policies, and consider Health Savings Accounts (HSAs) if you are still eligible and have a high-deductible health plan. HSAs offer a triple tax advantage and can be a powerful tool for healthcare savings in retirement.

4. Debt Management

High-interest debt can be particularly corrosive during inflationary periods. While inflation can, in theory, make fixed-rate debt cheaper in real terms over time, the burden of servicing that debt reduces the cash flow available for other expenses and investments.

- Pay Down High-Interest Debt: Prioritize paying off credit card debt, personal loans, and other high-interest obligations. This frees up cash flow and reduces financial stress.

- Review Mortgage: If you have a variable-rate mortgage, consider refinancing to a fixed rate if interest rates are favorable, to lock in predictable payments against potential future rate hikes by central banks combating inflation.

5. Long-Term Care Planning

The cost of long-term care is a significant concern for many retirees, and it tends to increase at rates often exceeding general inflation. Planning for this expense is crucial for safeguarding the rest of your retirement savings.

- Long-Term Care Insurance: Consider purchasing long-term care insurance. While premiums can be substantial, they can protect your assets from the potentially catastrophic costs of nursing home care or in-home assistance.

- Hybrid Policies: Some life insurance policies now offer long-term care riders, providing flexibility.

- Self-Funding: If your assets are substantial, you might consider self-funding, but understand the potential drain on your portfolio.

The Role of a Financial Advisor in Navigating 3.5% Inflation Retirement

Navigating the complexities of inflation and its impact on retirement savings can be daunting. A qualified financial advisor can be an invaluable partner in this process. They can help you:

- Assess Your Current Situation: A thorough review of your existing portfolio, income streams, and expenses.

- Develop an Inflation-Adjusted Plan: Create a personalized retirement plan that explicitly accounts for a 3.5% inflation retirement scenario and beyond.

- Optimize Your Investment Strategy: Recommend specific asset allocations and investments designed to outperform inflation while aligning with your risk tolerance.

- Identify Income Opportunities: Help you explore and optimize various income streams, including Social Security claiming strategies and annuity options.

- Stay Informed and Adapt: Provide ongoing guidance and adjustments to your plan as economic conditions evolve.

- Tax Efficiency: Advise on tax-efficient ways to draw income from your retirement accounts, especially important when inflation is high.

Psychological Impact of Inflation on Retirees

Beyond the purely financial implications, 3.5% inflation retirement scenarios can have a significant psychological toll on retirees. The fear of outliving one’s savings, the anxiety about rising costs, and the need to potentially adjust lifestyle expectations can be stressful. Financial advisors can also play a role in providing reassurance and helping clients maintain a realistic, yet optimistic, outlook.

It’s important to differentiate between nominal returns and real returns. A portfolio showing a 5% nominal gain when inflation is 3.5% is only providing a 1.5% real gain. This distinction is crucial for understanding the true growth of your wealth. Retirees often focus on the absolute dollar amount in their accounts, but the purchasing power of those dollars is what truly matters for their quality of life.

Staying Informed and Proactive

The economic landscape is constantly shifting. Staying informed about inflation trends, interest rate policies, and global economic developments is crucial. However, don’t let every news headline dictate hasty decisions. Instead, use information to have informed discussions with your financial advisor and make well-thought-out adjustments to your plan.

Review your retirement plan annually, or even more frequently if significant economic changes occur. This includes re-evaluating your budget, investment performance, and income needs. Proactivity is your best defense against the erosive effects of inflation.

Case Study: The Smiths and 3.5% Inflation

Let’s consider John and Jane Smith, who retired in late 2025 with a portfolio aiming to provide $60,000 in annual income. Their initial plan assumed a long-term average inflation of 2%. However, with 3.5% inflation retirement becoming a reality in early 2026, their purchasing power quickly began to erode.

After one year at 3.5% inflation, their $60,000 would only buy what $57,971 would have bought at retirement. If they continued on their original plan, their lifestyle would gradually decline. Recognizing this, they consulted their financial advisor. Their advisor suggested several adjustments:

- Portfolio Shift: Increased allocation to TIPS and a diversified REIT fund, reducing some exposure to lower-growth bond funds.

- Income Optimization: John, who had delayed claiming Social Security until 70, was now receiving higher, inflation-adjusted payments. Jane started a part-time consulting gig for 10 hours a week, bringing in supplementary income.

- Budget Review: They meticulously reviewed their expenses, cutting out a few discretionary subscriptions and negotiating a better rate on their home insurance.

- Healthcare Strategy: They explored different Medicare Advantage plans to find one that better suited their evolving healthcare needs and budget.

These proactive steps allowed the Smiths to mitigate the impact of 3.5% inflation, preserving their desired lifestyle and providing greater financial security. This case highlights the importance of not just having a plan, but also having the flexibility and willingness to adapt it when economic conditions change.

Conclusion: Empowering Your Retirement Against Inflation

The prospect of 3.5% inflation retirement in early 2026 is a significant factor that demands attention from current and future retirees. While inflation is a natural part of any economy, its impact on fixed incomes and long-term savings cannot be underestimated. By understanding its mechanisms, proactively adjusting your investment portfolio, optimizing income streams, diligently managing expenses, and planning for significant costs like healthcare and long-term care, you can build a more resilient retirement strategy.

Remember, the goal isn’t just to accumulate a large sum of money, but to ensure that sum retains its purchasing power throughout your retirement years. Engaging with a trusted financial advisor can provide the expertise and personalized guidance needed to navigate these economic waters successfully. Take control of your financial future today, and ensure your retirement dreams remain vibrant and secure, even in the face of rising costs.

Proactive planning and informed decision-making are your strongest allies in safeguarding your retirement savings against the silent erosion of inflation. Don’t wait for its full impact to be felt; act now to protect your peace of mind and financial well-being well into the future.