Understanding your healthcare costs is paramount, especially as you approach or enter retirement. For millions of Americans, Medicare Part B is a crucial component of their healthcare coverage, providing insurance for doctor’s services, outpatient care, medical supplies, and preventive services. As we look ahead to 2026, many beneficiaries are naturally wondering: What will happen with Medicare Part B Premiums? This comprehensive guide will delve into the anticipated landscape of Medicare Part B Premiums for 2026, the factors that influence these costs, and, most importantly, actionable strategies you can employ to potentially save money.

Navigating the complexities of Medicare can often feel like a daunting task. The rules, regulations, and costs can change annually, making it essential to stay informed. Our goal with this article is to demystify Medicare Part B Premiums, providing you with the knowledge and tools to plan effectively and make informed decisions about your healthcare future. By understanding the potential changes and available options, you can better manage your budget and ensure you receive the care you need without unnecessary financial burden.

The Basics of Medicare Part B Premiums

Before we dive into 2026 projections, let’s establish a foundational understanding of Medicare Part B Premiums. Medicare Part B covers medically necessary services and preventive services. Unlike Part A (Hospital Insurance), which most people don’t pay a monthly premium for if they or their spouse paid Medicare taxes for a specified period, Part B usually comes with a monthly premium. This premium is typically deducted directly from your Social Security benefit payment, if you receive one. If you don’t receive Social Security benefits, or your benefits aren’t enough to cover the premium, you’ll receive a bill from Medicare.

Who Pays Medicare Part B Premiums?

Generally, everyone enrolled in Medicare Part B pays a monthly premium. However, the amount varies based on several factors, most notably your income. This income-related adjustment is known as the Income-Related Monthly Adjustment Amount (IRMAA), which we will explore in detail.

What Does the Part B Premium Cover?

The Medicare Part B Premium contributes to the cost of a wide range of outpatient medical services. These include, but are not limited to:

- Doctor’s visits (both in-office and telemedicine)

- Outpatient hospital care

- Preventive services (e.g., flu shots, certain screenings)

- Medical equipment (e.g., wheelchairs, walkers)

- Laboratory tests

- X-rays and other diagnostic imaging

- Mental health services (outpatient)

- Ambulance services

It’s important to remember that even with the premium, Part B typically has an annual deductible, and after the deductible is met, you usually pay 20% of the Medicare-approved amount for most doctor’s services, outpatient therapy, and durable medical equipment, without a cap on out-of-pocket costs unless you have supplemental coverage.

Factors Influencing Medicare Part B Premiums for 2026

Predicting the exact Medicare Part B Premiums for 2026 is challenging, as the Centers for Medicare & Medicaid Services (CMS) typically announce these figures in the fall of the preceding year. However, we can identify several key factors that historically influence these premium adjustments. Understanding these factors provides insight into what beneficiaries might expect.

1. Healthcare Spending Trends

The overall cost of healthcare in the United States is a primary driver. Increases in the utilization of medical services, the cost of new medical technologies and drugs, and general inflation within the healthcare sector all contribute to rising expenditures for the Medicare program. If healthcare spending continues its upward trajectory, it’s reasonable to anticipate an increase in Medicare Part B Premiums.

2. Social Security Cost-of-Living Adjustment (COLA)

The Social Security Cost-of-Living Adjustment (COLA) plays a significant role, particularly due to the ‘hold harmless’ provision. This provision prevents a beneficiary’s net Social Security benefit from decreasing due to an increase in their Part B premium. If the COLA is substantial, it provides more headroom for Medicare to increase premiums without violating the hold harmless rule for a large portion of beneficiaries. A smaller or non-existent COLA can constrain premium increases for many.

3. Medicare Trust Fund Solvency

The financial health of the Supplementary Medical Insurance (SMI) Trust Fund, which pays for Part B and Part D benefits, is another critical factor. Actuarial projections about the trust fund’s solvency and future expenditures directly influence decisions regarding premiums. Policymakers aim to ensure the long-term stability of the program, which can sometimes necessitate premium adjustments.

4. Legislative and Regulatory Changes

Congressional action or new regulations from CMS can directly impact Medicare Part B Premiums. For instance, legislation aimed at reducing drug costs or expanding certain benefits could have downstream effects on premiums. While major legislative overhauls are less frequent, smaller adjustments can still occur.

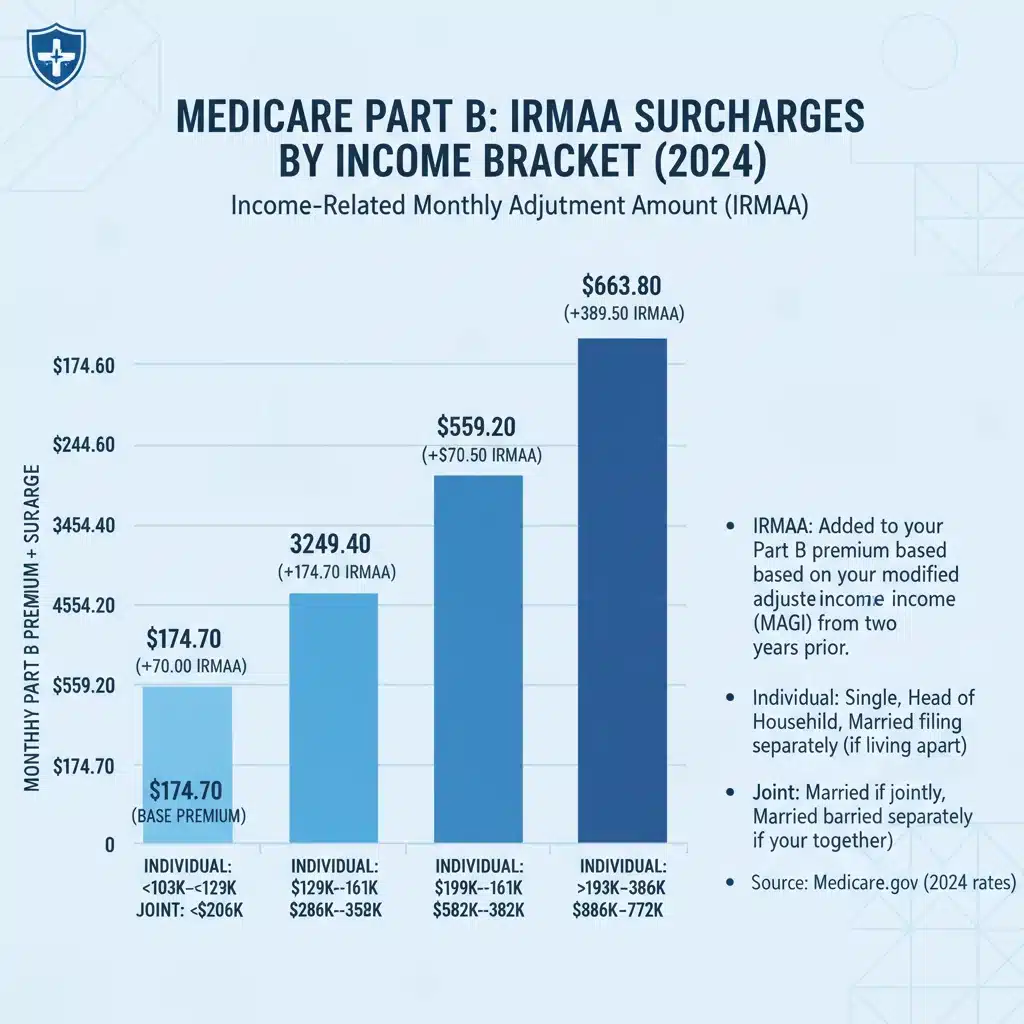

5. Income-Related Monthly Adjustment Amount (IRMAA) Thresholds

For higher-income beneficiaries, IRMAA means paying a higher Part B premium. The income thresholds for IRMAA are adjusted annually. Changes to these thresholds, or the percentages applied at each tier, will directly affect how many people pay IRMAA and how much they pay. We’ll delve deeper into IRMAA shortly.

Projected Outlook for Medicare Part B Premiums in 2026

While specific numbers for 2026 are not yet available, historical trends and current economic indicators suggest a likelihood of continued increases in Medicare Part B Premiums. Healthcare inflation, the introduction of new, often expensive, medical treatments, and the ongoing demand for services by a growing senior population all point towards an upward trend.

In recent years, we’ve seen significant fluctuations. For example, some years have seen substantial increases, while others have been more modest, sometimes even a slight decrease. These shifts are often tied to specific events, such as the initial coverage of a new expensive drug or legislative interventions. Beneficiaries should mentally prepare for a potential increase and begin exploring strategies to mitigate these costs.

Understanding IRMAA: Income-Related Monthly Adjustment Amount

For many, the standard Medicare Part B Premium is what they pay. However, if your modified adjusted gross income (MAGI) exceeds certain thresholds, you will pay an Income-Related Monthly Adjustment Amount (IRMAA) in addition to the standard premium. This means higher-income beneficiaries pay a larger share of their Part B costs.

How IRMAA is Determined

IRMAA is based on your MAGI from two years prior. So, for 2026 Medicare Part B Premiums, the Social Security Administration (SSA) will typically look at your 2024 tax return. MAGI includes your adjusted gross income (AGI) plus tax-exempt interest income.

IRMAA Brackets (Illustrative, based on current structure)

While the exact dollar amounts for 2026 IRMAA brackets will be released later, the structure generally involves several income tiers. As your income crosses each threshold, your Part B premium increases. It’s crucial to understand these brackets, as even a slight increase in income can push you into a higher IRMAA tier, significantly increasing your Medicare Part B Premiums.

For example, if the 2026 standard premium is X, and the first IRMAA threshold is Y, then individuals or couples earning above Y would pay X plus an additional surcharge. Subsequent tiers would add further surcharges. This is why income planning is a vital strategy for managing Medicare costs.

Strategies to Potentially Save on Medicare Part B Premiums

Even with potential increases in Medicare Part B Premiums, there are several proactive steps you can take to manage or even reduce your costs. These strategies range from income planning to exploring alternative coverage options.

1. Income Planning to Avoid or Reduce IRMAA

Since IRMAA is based on your income from two years prior, you have a window of opportunity to plan. If you anticipate your income for a future year (e.g., 2024 for 2026 premiums) might push you into an IRMAA bracket, consider strategies to reduce your MAGI. This could include:

- Tax-Efficient Retirement Withdrawals: Strategically withdrawing from different types of retirement accounts (e.g., Roth vs. traditional IRAs/401ks) can impact your MAGI. Roth withdrawals are generally tax-free and don’t count towards MAGI for IRMAA purposes.

- Qualified Charitable Distributions (QCDs): If you are 70½ or older, you can make direct transfers from your IRA to a qualified charity. These QCDs count towards your Required Minimum Distributions (RMDs) but are excluded from your MAGI, potentially lowering your IRMAA.

- Delaying Large Capital Gains: If you plan to sell significant assets, consider the timing to avoid an unusually high-income year that could trigger IRMAA for two years down the line.

- Managing Other Income Sources: Be mindful of how other income, such as rental income, business profits, or taxable investments, contributes to your MAGI.

Consulting with a financial advisor specializing in retirement planning and Medicare can be invaluable for developing a personalized income strategy.

2. Exploring Medicare Advantage Plans (Part C)

Medicare Advantage plans, offered by private insurance companies approved by Medicare, must cover everything Original Medicare (Part A and Part B) covers. Many Medicare Advantage plans offer additional benefits not covered by Original Medicare, such as vision, dental, hearing, and prescription drug coverage (Part D).

Crucially, many Medicare Advantage plans have a $0 monthly premium *beyond* your standard Medicare Part B Premium. Some plans even offer a Part B premium reduction, where the plan pays a portion of your Part B premium. This can be a significant saving for beneficiaries. However, it’s essential to understand that Medicare Advantage plans often have their own network restrictions, referral requirements, and different cost-sharing structures (copayments, deductibles, out-of-pocket maximums) compared to Original Medicare.

3. Considering Medigap (Medicare Supplement Insurance)

Medigap policies are sold by private companies and help pay some of the healthcare costs that Original Medicare doesn’t cover, like copayments, coinsurance, and deductibles. While Medigap policies have their own monthly premiums, they can significantly reduce your out-of-pocket costs for Part A and Part B services. For individuals who frequently use medical services, a Medigap plan, combined with Original Medicare, might offer more predictable costs than relying solely on Original Medicare with its 20% coinsurance without an out-of-pocket limit.

It’s important to note that you cannot have both a Medicare Advantage plan and a Medigap policy simultaneously. You must choose one path. If you choose Original Medicare and Medigap, you will still pay your Medicare Part B Premium, plus the Medigap premium.

4. Medicare Savings Programs (MSPs)

For individuals with limited income and resources, Medicare Savings Programs (MSPs) can help cover some or all of your Medicare costs, including Medicare Part B Premiums. These programs are administered by your state and can significantly reduce your healthcare burden. There are different types of MSPs, each with varying income and resource limits:

- Qualified Medicare Beneficiary (QMB) Program: Helps pay for Part A and Part B premiums, deductibles, coinsurance, and copayments.

- Specified Low-Income Medicare Beneficiary (SLMB) Program: Helps pay for Part B premiums.

- Qualifying Individual (QI) Program: Helps pay for Part B premiums.

- Qualified Disabled and Working Individuals (QDWI) Program: Helps pay for Part A premiums for certain disabled individuals.

If you believe you might qualify, it’s highly recommended to contact your state’s Medicaid office or State Health Insurance Assistance Program (SHIP) for more information and to apply. Even a small amount of assistance can make a big difference in managing your Medicare Part B Premiums.

5. Utilizing Preventive Services

While not directly reducing your Medicare Part B Premiums, taking advantage of Medicare’s covered preventive services can help you stay healthier and potentially avoid more costly medical issues down the line. Many preventive services are covered 100% by Part B, meaning no copayment or deductible applies if you use a Medicare-approved provider. Regular check-ups, screenings, and vaccinations are crucial for early detection and management of health conditions, ultimately leading to better health outcomes and potentially fewer overall healthcare expenses.

6. Annual Medicare Plan Review

Each year during the Annual Enrollment Period (AEP), typically from October 15 to December 7, you have the opportunity to review your Medicare coverage. This is a critical time to assess whether your current plan still meets your needs and budget. Premiums, deductibles, copayments, and formularies (for Part D) can change annually. Comparing plans, including Medicare Advantage and Part D plans, can help you find coverage that offers the best value and potentially lower overall costs, even if your Medicare Part B Premiums increase.

Preparing for 2026: A Checklist

As 2026 approaches, here’s a simple checklist to help you prepare for potential changes in Medicare Part B Premiums:

- Review Your 2024 Income: Understand how your Modified Adjusted Gross Income (MAGI) from 2024 could impact your 2026 IRMAA.

- Consult a Financial Advisor: Discuss strategies for tax-efficient income planning to mitigate IRMAA.

- Stay Informed: Keep an eye on announcements from CMS and the Social Security Administration regarding 2026 Medicare costs, typically released in the fall of 2025.

- Evaluate Your Current Coverage: During the next AEP, thoroughly review your Medicare Advantage or Medigap plan to ensure it’s still the best fit.

- Explore Medicare Savings Programs: If your income and resources are limited, investigate if you qualify for state-based assistance.

- Utilize Preventive Care: Take advantage of covered preventive services to maintain your health and avoid future high costs.

The Role of Advocacy and Future Outlook

The cost of healthcare, including Medicare Part B Premiums, is a continuous topic of discussion among policymakers, advocacy groups, and the public. Efforts to control healthcare costs, improve efficiency, and ensure the long-term sustainability of Medicare are ongoing. Beneficiaries and their advocates often play a crucial role in raising awareness about the impact of rising premiums on seniors and individuals with disabilities.

Future legislative changes could aim to reform how Medicare is funded, how drug prices are negotiated, or how services are delivered. These changes, if enacted, could have a significant impact on Medicare Part B Premiums in the years to come. Staying engaged and informed about these broader discussions can also help you understand the context behind premium adjustments.

Conclusion: Proactive Planning is Key

While the exact figures for Medicare Part B Premiums in 2026 remain to be seen, a proactive approach to understanding the factors at play and exploring available savings strategies is your best defense against unexpected costs. By planning your income, carefully reviewing your coverage options, and leveraging available assistance programs, you can navigate the complexities of Medicare with greater confidence and financial security.

Don’t wait until the last minute to assess your situation. Start now by reviewing your income, understanding your current plan, and seeking professional advice if needed. Being well-informed and strategic about your Medicare choices will empower you to manage your healthcare expenses effectively, ensuring you receive the care you need without undue financial stress. The future of your healthcare starts with informed decisions today, especially concerning your Medicare Part B Premiums.

to $23,000 for 2025 Retirement Planning")